How does the Congress Stimulus Packages affect you?

During this difficult and uncertain time, we know you have many questions and concerns. TAPS has been working diligently to provide you the answers.

Here is what we know so far…

-

On April 21 and 23 respectively, the U.S. Senate and House of Representatives passed the Paycheck Protection Program and Health Care Enhancement Act and the President signed it into law on April 24, 2020. The bill provides $484 billion in additional funding for the Paycheck Protection Program (PPP), small business disaster loans and grants, hospitals and health care providers and testing.

Here are the major funding items of the fourth stimulus package.

-

On March 25, 2020, the Senate unanimously passed a $2.2 trillion Coronavirus Aid, Relief, and Economic Security Act - CARES Act. The House passed the bill on March 27 and President Trump promptly signed it into law. This bill is the third large-scale congressional effort in response to the novel coronavirus (COVID-19) outbreak.

After going through the 880-page bill, here are the key CARES act take-a-ways we believe affect our TAPS community the most.

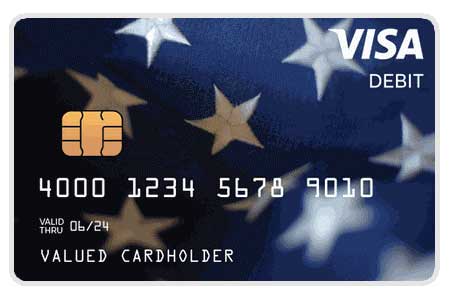

- Some CARES Act payments are being sent by prepaid debit cards. Get the details on what the card looks like and how to access your payment.

Why a fourth stimulus bill and what exactly does it cover?

Small Business Paycheck Protection Program (PPP)

Unfortunately, small businesses have been hit hard by state recommended closings to ensure public safety during the coronavirus crisis. Many small businesses applied for the Paycheck Protection Program (PPP) loans granted under the CARES Act. However, the $350 billion set aside for this program was depleted within just two weeks.

The bill provides an additional:

- $310 billion in PPP funding for small businesses

- $60 billion to aid small, midsize, minority and community lenders

Disaster Loans Program

Small businesses that have suffered “substantial economic injury” as a direct result of COVID-19 may be eligible for further relief.

The bill provides an additional:

- $50 billion for the Disaster Loans Program

- $10 billion for Emergency Economic Injury Disaster Loan (EIDL) Grants

Hospital and Healthcare Provider Grants

Hospitals and healthcare providers in our communities have been on the frontlines in the fight against the coronavirus pandemic.

The bill provides an additional:

- $75 billion in financial relief to hospitals and healthcare providers

Testing

Researchers have called for more testing before reopening the country. The bill requires the Administration to create a national strategy to provide assistance to states for testing and increasing testing capacity.

The bill provides:

- $25 billion to research, develop, validate, manufacture, purchase, administer and expand capacity for COVID-19 tests

The CARES Act Provides:

Critical financial relief through direct payments to individuals and families

The measure provides for a one-time tax rebate for as much as $1,200 per individual, $2,400 per couple and $500 per eligible child. It is not reduced for lower income Americans but is reduced for higher income earners, starting at $75,000 for individuals, $112,500 for head of household, and $150,000 for married couples. The credit would be reduced by 5% for the amount a taxpayer’s income exceeds the threshold. It phases out completely at $99,000 for individuals and $198,000 for married couples.

How do you know if you will receive a tax rebate?

The rebate is based on 2019 taxes, or for individuals who haven’t filed, against their 2018 taxes or 2019 Social Security statements. Payments would be made through December 31, 2020. Rebates will be delivered electronically to accounts where a taxpayer authorized deposit of a tax refund or other federal payment on or after January 1, 2018. Notices will be sent to taxpayers within 15 days of sending the payment. A Social Security number will be required to claim the rebate.

- $75,000 or less will receive the full amount of $1,200

- Between $75,000 – $99,000, the credit is reduced by 5% for the amount a taxpayer exceeds the threshold

- It phases out completely at $99,000

- $112,000 or less will receive the full amount of $1,200

- $150,000 or less will receive the full amount of $2,400

- Between $150,000 – $198,000, the credit is reduced by 5% for the amount the taxpayers exceed the threshold

- It phases out completely at $198,000

- You must claim them as a dependent on your tax return

- They must be under age 17

- They must be related to you (blood, marriage, or adoption)

- They can’t provide more than half of their financial support during the tax year

- They must be a U.S. citizen, a U.S. national or a U.S. resident alien

- They must live with you for at least half of the year

- If you claimed a child under 17 as a dependent on your most recent filed tax return (2018 or 2019), they are not eligible to receive the $1,200 stimulus payment

- If you claimed your child as a dependent and they filed their own tax return, they will only be eligible for the $500 payment if they meet the requirements

- Dependent children ages 17-18 or a full-time student through age 24 do not qualify for the $500 stimulus payment

- SSI recipients will receive the full $1,200 economic impact payment

- You will not need to file a tax return to get the payment

- Payments will be automatically deposited into your bank accounts or sent by mail – however you typically receive your benefits

- The IRS projects the payments for this group will go out no later than early May

Emergency loans to small businesses so that they can keep paying their workers

Small businesses have been severely impacted by state-imposed closures to stop the spread of the coronavirus. Loans backed by the Small Business Administration (SBA) will help small businesses, nonprofits, veterans groups, and tribal businesses with 500 or fewer employees, independent contractors, and eligible self-employed workers pay for expenses. Loans taken by small businesses and nonprofits to keep employees on payroll may be forgiven as well.

Employers of all sizes that face closure orders or suffer economic hardship due to the COVID-19 crisis that continue to pay furloughed employees may be eligible for a 50% credit on up to $10,000 of wages paid to those employees.

What does this mean for you?

If you are currently employed full time or part time by a small business or nonprofit, this will help you to keep your job, help local businesses ride out this storm, and ensure that furloughed workers have jobs to return to.

If you are a small business owner, independent contractor or self-employed, it will enable you to apply for a much-needed loan.

Expanded unemployment benefits for workers during the health care crisis

State unemployment offices are experiencing an unprecedented spike in claims and many workers are not covered under regular state unemployment laws. The CARES Act provides economic relief and much-needed support for workers by making a significant investment in unemployment benefits.

It makes benefits more generous by adding a $600 a week across-the-board payment increase through the end of July. In addition, for those who need it, the bill provides an additional 13 weeks of benefits beyond what states typically allow. The expansion in unemployment benefits expires at the end of 2020 in recognition of the temporary nature of this current crisis.

The bill also includes support to state and local governments and nonprofits so they can pay unemployment to their employees.

Unemployment insurance is a joint state-federal program that provides cash benefits to eligible workers. Each state administers a separate unemployment insurance program, but all states follow the same guidelines established by federal law.

How do you file a claim for unemployment benefits?

There are two primary steps to receiving unemployment insurance. First you must file an application to establish or reopen a claim. If you are out of work due to the Coronavirus crisis then you will select “Lack of Work” as the reason for separation. Secondly, you access the program each week to claim unemployment insurance payment.

You can file your application or reopen your previous claim by visiting your state’s employment commission website.

Student loan forgiveness

With the closing of universities and colleges across our country, many students are faced with unpaid student loans. The U.S. Department of Education (DoEd) has temporarily set the interest rate on all federally held student loans to 0%. These loans will be automatically put in forbearance through September 2020.

There is no impact at this time on private student loans. Students may contact their loan servicer to attempt to defer but do not have any rights in this regards the way they do with federal student loans.

DoEd has asked all collection agencies to stop attempting to collect on defaulted student loans indefinitely. In addition, the federal government cannot garnish stimulus checks due to outstanding debt, including defaulted student loans.

Who should you contact to make sure your student loans have been put in forbearance?

Students should contact their “loan servicer” – the company you pay each month – to confirm your loans have been put in forbearance. This special administrative forbearance allows you to stop making monthly payments but still be counted as making qualifying payments towards Public Service Loan Forgiveness (PSLF) or Income-Driven Repayment (IDR).

If you chose to defer your payments completely during this time, those do not count towards PSLF. Recommend using forbearance of income driven repayment (payments as low as $0 per month) over deferment at this time.

Are GI Bill and Fry Scholarships impacted?

We are waiting for guidance from DoEd on how direct grants to Institutions of Higher Learning (IHL) would work and if GI Bill and Fry Scholarship recipients would be impacted. Generally, we know they will provide direct aid to students whose attendance was disrupted to include refunding room and board fees, moving off campus, finding emergency housing, childcare needs, and healthcare.

Essential investments in new medicines and vaccines to fight this deadly virus and to get the equipment our brave medical professionals need

Increases the Medicare reimbursement rate to assist providers caring for our most vulnerable population. It also increases access to testing by allowing the Strategic National Stockpile to stockpile swabs necessary for test kits. Allows the U.S. Food and Drug Administration (FDA) to quickly approve the use of new medication and treatments. Facilitates the use of new and innovative telemedicine technology to protect and contain the spread of COVID-19.

How does this help my family?

Whether you receive care in a VA hospital, Military Treatment Facility (MTF), or through a civilian provider, these essential investments help ensure access to care for all Americans.

Economic Impact Payments Sent by Prepaid Debit Cards

Nearly 4 million people are being sent their Economic Impact Payment by prepaid debit card, instead of paper check. The debit cards arrive in a plain envelope from "Money Network Cardholder Services." Unfortunately, we are hearing that some people are confusing them with unsolicited credit card offers and are accidentally throwing them out or shredding them.

Why am I receiving a debit card?

If you are a taxpayer who filed your 2018 or 2019 taxes with the Internal Revenue Service (IRS), but did not provide your banking information to allow for direct deposit.

How do I identify my debit card?

The IRS has stated that the debit cards bear the VISA logo and are issued by MetaBank. A letter included with the cards explains that they are the Economic Impact Payment (EIP) Card. The EIP Card is sponsored by the Treasury Department’s Bureau of Fiscal Service as part of the U.S. Debit Card Program.

What if I destroyed my debit card?

You can request a new one by calling the customer service line at 800-240-8100 and can visit the EIP website for additional information.

How do I activate my debit card?

Once you receive your card, you can activate it by calling the same customer service line, 800-240-8100, and providing your name, address, and social security number. Activators will then be asked to create a unique four-digit PIN in order to make ATM withdrawals or check their balance.

Card holders can also create an account on the EIP website that allows them to check their balance and transaction history without having to call the customer service line.

How do I protect my debit card?

Make sure you have a secure PIN, and don’t give it to anyone. Beware of online phishing scams trying to get your card number and PIN. If you think someone has made an unauthorized purchase, call the toll-free number at 800-240-8100.

If you have any further questions, please email policy@taps.org or call 800-959-8277 (TAPS).